The basic goal of estate and gift tax planning is to ensure that as much of your assets and property, whether they are gifted during your lifetime or bequeathed in your Will, are transferred with as little taxation consequences as possible.

With careful estate and tax planning, it is possible to minimize or even eliminate the amount of tax payable on the transfer of your assets to your loved ones.

Small Gift Exception

Under the Small Gift Exemption you can give a gift up to the value of €3,000 to any person in a calendar year without having to pay Capital Gains Tax (CAT). You may also take a gift from several people in the same calendar year and the first €3,000 from each person is exempt from CAT (Capitial Acquisition Tax). Gifts within this limit are not taken into account in computing tax and are not included for aggregation purposes. It’s well worth utilising this annual exemption from gift tax as part of your inheritance planning strategy, especially since gift and inheritance tax is levied at a rate of 33%.

Making use of the Small Gift Tax Exemption

Are you thinking of setting up a savings plan for your children, a niece, nephew or Godchild? Make use of the annual small gift tax exemption by setting up a regular saving plan to which you make a regular monthly or annual contribution. This is invested in your chosen fund from a range of funds available in the market. The fund selection will apply for the life of the plan. To ensure these savings maximise the Gift Tax Exemption for the child, you must legally assign the plan to that child. By assigning the plan over, the child will be entitled to the proceeds of the policy tax-free because they are the owner of the plan as assignees.

Gift Tax Planning

Under the small gift exemption a person can take a gift from several people in the same calendar year. The first €3,000 from each person is exempt from CAT. So if you’re thinking of helping your son or daughter and their respective partners with a deposit for a house – if it is done right, four parents (his and hers) could gift a couple €48,000 in total without a tax implication over the two months (December and January).

While there is no limit on who can give to whom under the small gift exemption. You could, technically, give to neighbours, friends or even perfect strangers if your funds allowed and the fancy took you. There are two restrictions:

- You can only gift a maximum of the €3,000 to any one person in any one tax year. And it doesn’t have to be in one payment – you could, for instance, make 10 payments of €300.

- The second rule is the one where you will find Revenue getting picky. The gift must be for the benefit of the person receiving it. For instance, if you gave this son €3,000 and then gave someone else €3,000 with the intention that they, too, would give it to your son, Revenue would not be at all happy.

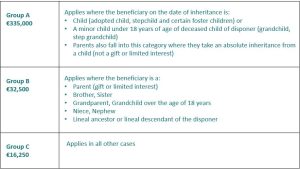

Section 73 – Gift Tax Exemption

If you wish to leave a gift over and above the threshold careful Tax Planning is required to minimize your family’s inheritance / gift tax liability so that as much of your wealth as is possible passes to your beneficiaries. To avoid a hefty tax liability, should you decide to pass on your assets during your lifetime, you can set up a Section 73 Savings Policy, recognised by Revenue, to pay this gift tax liability if it’s above the annual exemption threshold of €3,000. This allows your assets to be transferred and utilised sooner whilst providing a substantial saving for your beneficiary. In addition, any further growth in value of assets after the transfer falls outside the CAT regime.

This Revenue approved savings plan can be set up for anyone who has assets that they want to transfer to their children (or other beneficiaries) during their lifetime. The relief allows people to plan for the payment of gift tax in a tax efficient way, but if you decide not to utilise it for this purpose you still have savings to use however you wish. Furthermore, if a Section 73 savings plan is put in place to provide for the payment of gift tax, Revenue will not charge Capital Acquisitions Tax on the plan proceeds if the money is actually used to pay gift tax.

If you would like to know more about the Small Gift Exemption, Inheritance Tax Planning or general Estate Planning so you can minimise your tax burden, click the ‘request a chat’ button below to schedule an appointment.

This is for information purposes only and should not be used or interpreted as financial advice. You should always obtain your own independent financial, tax and legal advice based on your own particular circumstances, before entering into any financial contract.